Why you should think about your exit now

The exit is a critical step in the lifetime of almost any Life Science product, in order to deliver on the company’s mission and make a big impact on the treatment and quality of life of patients around the world. While it may feel counterintuitive to think of an exit while developing an innovation, it is essential to be aware of the various options that exits provide. This will enable you to steer swiftly when you find yourself in unexpected situations that will occur over the 10-year+ development cycle of the product. In this series of articles, we discuss the different exit strategies for Life Science innovations, share key insights, and ensure you can make an informed decision to push your innovation to market.

At FFUND we are strong believers in planning for success and being ready when the opportunity arises at the horizon. In this article, the last in our “prepare for success – exit deals” series, we highlight the payment terms for the various deal-types that you may be facing when developing a Life Sciences product. When entering an exit deal, it’s crucial to evaluate its effect on your company’s cash position, the product’s prospects for success, and the personal impact it may have. Understanding these factors is essential for a well-informed negotiation.

Payment schemes for exit deals in Life Sciences

#1 Licensing deals and technology transfer

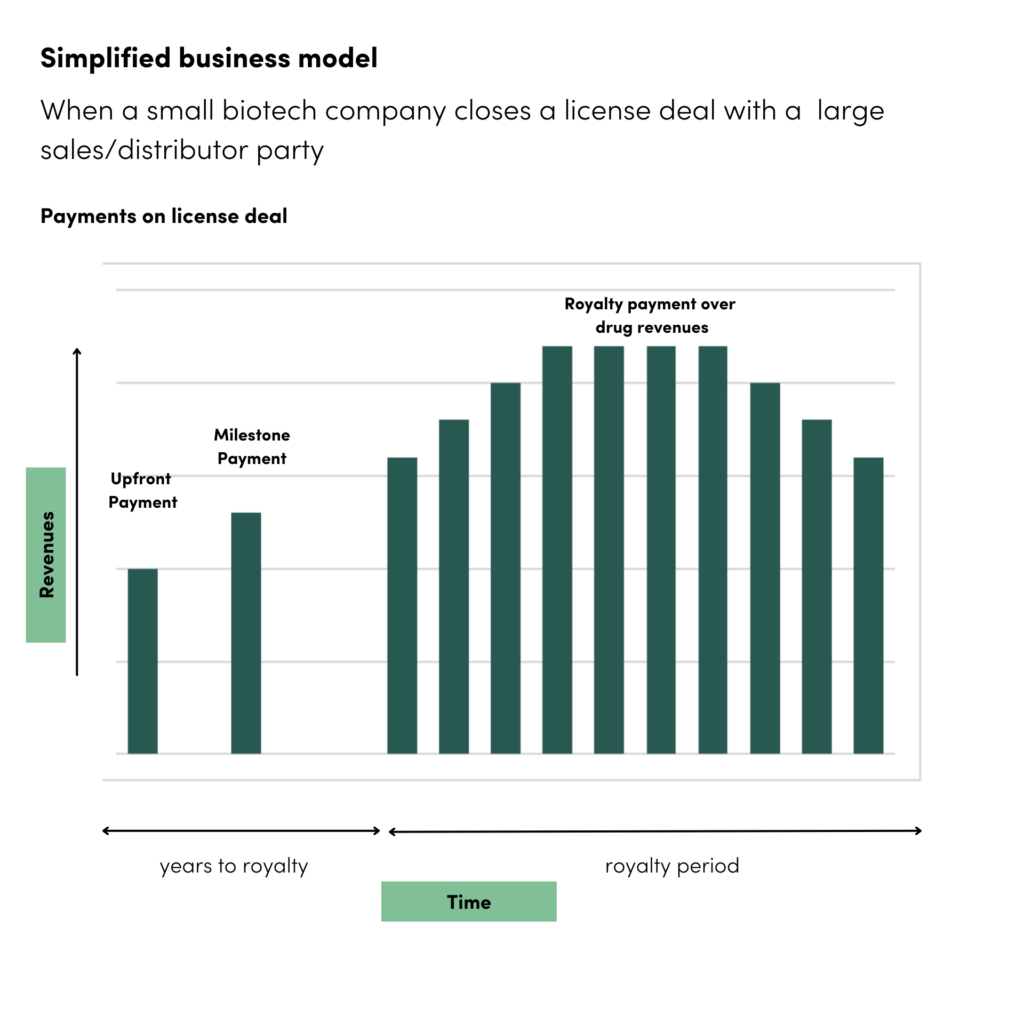

The payment terms in a licensing deal in the Life Sciences industry can vary depending on the specific circumstances, the value of the intellectual property (IP), and development stage of the technology. Frequently, a combination of the following payment conditions is seen:

- Upfront payments: It is common for a licensing deal to involve an upfront payment, also known as an initial license fee. This is a one-time payment made by the licensee to the licensor upon execution of the agreement. The amount can vary significantly and is typically based on factors such as the value of the IP, the stage of development, market potential, and bargaining power of the parties.

- Milestone payments: These are additional payments, which are included in many life sciences licensing deals, made by the licensee to the licensor upon achieving specific predefined milestones. Milestones can be related to various factors such as successful completion of clinical trials, regulatory approvals, commercialization milestones (e.g., reaching certain sales targets), or other agreed-upon events. The timing and amount of milestone payments are typically negotiated and stated in the licensing agreement.

- Royalties: Royalties are ongoing payments made by the licensee to the licensor based on a percentage of the revenue generated from the licensed technology or product. The royalty rate can vary but is commonly negotiated based on factors such as the market, competition, and the value of the IP.

- Equity or equity-related considerations: In some licensing deals, especially in early-stage or technology-driven companies, the licensor may receive equity in the licensee company as part of the payment. This can align the interests of both parties and provide the licensor with potential upside if the licensee becomes successful.

#2 Management buyout (MBO)

In an MBO, the management team typically assembles the necessary financing, either through personal funds, bank loans, or investment from external sources, to acquire the ownership stake. Factors such as the financial condition of the company, the perceived value of the business, the risk profile, and the bargaining power of each party can all influence the payment terms in an MBO deal. Next to a direct payment for the MBO by the new owners to the previous owners, the payment terms may include:

- Seller financing: The purchase price is paid over time directly to the sellers. In such cases, seller financing terms, such as interest rates, repayment terms, and security arrangements, are negotiated between the parties.

- Earnouts: An earnout arrangement is used when there is uncertainty regarding the future performance or value of the company. Under an earnout, a portion of the purchase price is tied to the future financial performance of the company.

- Contingent payments: Contingent payments, also known as contingent consideration or deferred consideration, are made to the sellers based on the achievement of specific future events or milestones, such as successful product launches, regulatory approvals, or business performance targets.

#3 Merger & acquisition (M&A)

M&As may include various deal terms, depending on the business development level and Technology Readiness Level (TRL), as well as the market potential of the companies that are part of the deal. In M&As the following payment forms are seen:

- Cash payment: Cash is one of the most common forms of payment in an M&A deal. The acquiring company pays a certain amount of cash to the shareholders of the target company in exchange for their shares. The cash payment can be made upfront or in installments, based on the terms agreed upon in the acquisition agreement.

- Stock payment: In some cases, the acquiring company may offer its own shares as consideration for the acquisition. The value of the shares is typically determined based on a predetermined exchange ratio or the prevailing market price at the time of the transaction.

- Earnouts: An earnout arrangement may be included in the payment terms of an M&A deal, particularly when there is uncertainty regarding the future performance or value of the target company. Under an earnout, a portion of the purchase price is tied to the achievement of specific future financial or operational milestones.

- Debt assumption: In some cases, the acquiring company may assume the target company’s existing debt obligations as part of the acquisition. The acquiring company takes on the responsibility of repaying the assumed debt after the completion of the transaction.

- Contingent payments: Contingent payments may be included in the payment terms of an M&A deal. These payments are made to the sellers of the target company based on the achievement of specific future events or milestones, such as successful product launches, regulatory approvals, or business performance targets.

#4 Initial Public Offering (IPO)

Going public through an IPO provides a company with the opportunity to raise significant capital by selling shares to public investors. This infusion of capital enhances the company’s liquidity position by increasing its cash reserves. While an IPO provides liquidity opportunities, the actual liquidity of a company’s shares will depend on demand and trading activity in the market, which obviously comes with certain risks when the solidity of the technology and the business would be insufficiently secured.

Finally, an IPO allows existing shareholders, such as founders, early investors, and employees, to monetize their investments and achieve liquidity. By going public, these shareholders can sell their shares on the public market, potentially realizing significant value. Liquidity events like an IPO provide an exit opportunity for early investors and may incentivize future investment in the company.

Conclusion

In sum, the different frequently seen exit strategies in Life Sciences have significant differences in terms of the payment schedules and cash position of the company and its owners. To ensure you close a good deal that aligns with your personal goals, as well as the business goals, read the previous articles in this series on i.e. how exits can increase the chances to make impact with your product and the impact of the different exit strategies.

Would you like to learn more about exit strategies?

In our series of articles on exits, we discuss the different exit strategies for Life Science entrepreneurs. Learn more about the key insights into the available exit strategies by reading the following articles:

This article is part of the series Exit Strategies for Life Science innovations cocreated by Victor Bakker and Judith Smit.